Partially supported by a NULab Seedling Grant.

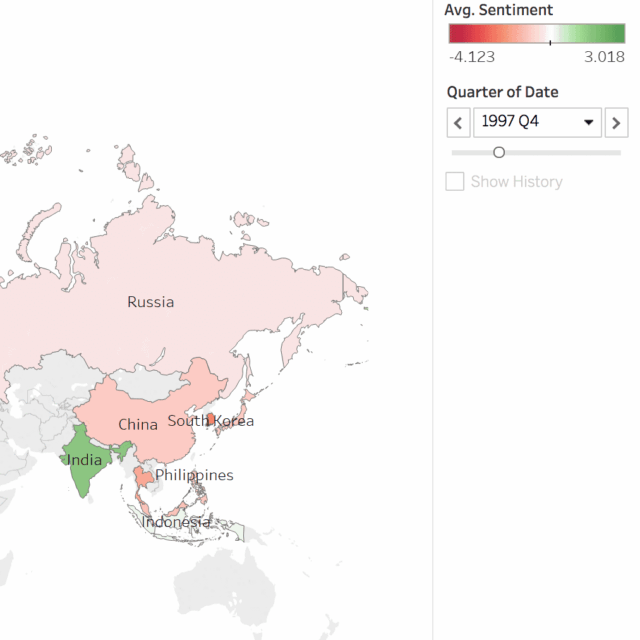

This project explores whether a real-time sentiment index, constructed using the universe of Reuters news, can help in forecasting GDP and predicting extreme events, such as large reversal in capital flows, in emerging markets.

Compared to traditional Early Warning Systems (EWS), a key advantage of a news based sentiment index is its availability in real-time at a daily frequency. This is especially relevant for emerging market countries in which macroeconomic data are available with more considerable lags and often subject to larger revisions than in advanced economies.

Our news sentiment index is built using “bag-of-words” text analysis techniques, which allow us to extract a summary measure of the intensity of positive or negative tonality in any written piece of news. In this approach, texts are split into words (or groups of words) disregarding sentence structures, and the positivity (negativity) of each (group of) words is assessed using dictionaries. The advantage of such an approach, over-optimizing machine learning techniques, is to make the classification transparent, easily replicable, and independent of the corpus of texts used. Our sentiment index is based on an exhaustive panel of about 2 million news articles from Reuters covering 12 emerging market countries over the period 1991—2015.

Assessing its predictive ability, we find that the news sentiment index systemically improves GDP forecast over that of Consensus forecasts, both in panel and country-by-country regression framework. The reduction in Root Mean Square Error (RMSE) over our benchmark, is, on average, 12% but can be considerably more for some countries. The news sentiment index also improves the forecasting ability of the traditional EWS model, both in fixed effect panel regressions and in country-by-country regressions. In particular, using the sentiment index, one could predict more accurately the sudden stops associated with the East Asian Crises of the late 1990s.

In addition to contributing to a recent and fast-growing literature which relates information extracted from text to economic and financial variables, this project contributes to the early warning signal literature and shows that exploiting information in big data—in particular in the mass of news and articles—can help institutions anticipate extreme events.

An interactive visualization is available here.

Principal Investigator

Samuel Fraiberger, Postdoctoral Research Associate, Network Science

Publications and Presentations

Research from this project has been presented at events such as the IMF Big Data and Analytics symposium and the NLP+CSS workshop at EMNLP 2016 (proceedings here).